Interactive infographic: Far North projects

Canada’s vast northern region hosts numerous large and high-grade mineral projects but they’re out of reach to miners until they’re connected to […]

There is a paradox at the heart of Canada’s relationship with its own territory. The country sits atop some of the most valuable mineral deposits on earth: uranium, nickel, copper, rare earths, zinc. And yet most of it remains untouched, not for lack of interest, but for lack of roads.

The Far North hosts world-class critical mineral projects stranded by distances that would dwarf the highway networks of entire European nations. Meanwhile, the geopolitical pressure on Canada to assert meaningful sovereignty over that same territory has never been greater.

These two facts are not unrelated. They are, in fact, the same problem.

As we reported on Wednesday this week, Chinese-owned mining giant MMG is positioned to benefit handsomely from the long-awaited Grays Bay Road and Port project in Nunavut.

That irony deserves a moment of reflection. A piece of infrastructure funded in part through Canadian public investment, designed to open up Canada’s Arctic to resource development, may do more in the near term to advance the interests of a Beijing-controlled company than to build a sovereign Canadian supply chain.

That is not an argument against Grays Bay, it is an argument for Canada to think much more strategically about what it is building, for whom and why.

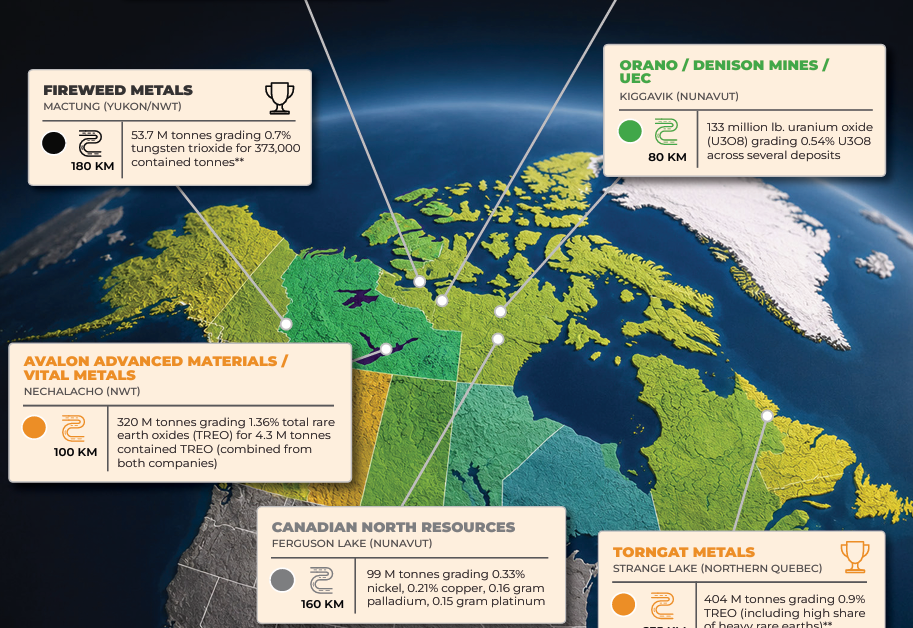

The case for Grays Bay and projects like it is overwhelming on its own terms. An infographic maps seven stranded mega-projects across the territories and northern Quebec, each one a potential economic engine, each one sitting beyond the end of the road.

MMG’s Izok Corridor in Nunavut holds 29 million tonnes grading 8.6% zinc and 2.4% copper — among the richest base metal deposits in the world — and sits 350 km from the nearest permanent road.

Glencore’s Hackett River silver-zinc deposit, Fireweed Metals’ Mactung tungsten project on the Yukon-N.W.T. border, the Kiggavik uranium deposits controlled by Orano, Denison and UEC, the vast rare earth resources at Nechalacho and Strange Lake — all of them are waiting for the same thing: a road.

Together they represent hundreds of billions of dollars in mineral value and, more critically, resources that allied nations are actively scrambling to secure from any jurisdiction they can find.

Canada has them. It just can’t get to them.

The infrastructure deficit in the Far North is not news. What is new is the urgency. The energy transition has supercharged demand for the very metals stranded in Canada’s Arctic. The AI buildout is driving electricity consumption that is reviving nuclear power globally, putting uranium back at the top of the strategic agenda.

Rare earths, once considered a Chinese monopoly, are now a declared national security priority in Washington, Brussels and Tokyo. And Canada’s own relationship with the United States, still navigating the aftershocks of tariff warfare and questions about continental economic integration, has made the argument for a sovereign Canadian critical minerals supply chain impossible to ignore at the Cabinet level.

So why is the map still dotted with projects going nowhere?

The honest answer is that Canada has consistently underinvested in northern infrastructure while treating each mining project as an isolated commercial proposition rather than a piece of a national strategic puzzle.

The Grays Bay Road and Port is one of the few initiatives that breaks that mould — a corridor concept that serves multiple deposits and multiple purposes, including the sovereign reality of putting Canadians to work in the Arctic. But it has been studied, reviewed, and deferred for decades. The pace of deliberation is not matched by the pace of global events.

The territories are not the only jurisdiction in this issue wrestling with the tension between resource development and regulatory uncertainty. In British Columbia, the mining industry has spent the better part of three years trying to understand what the province’s Declaration on the Rights of Indigenous Peoples Act means in practice for project approvals, a question Senior Writer Frédéric Tomesco examines closely in his story.

The answer matters enormously, not just for B.C.’s copper and gold sector but as a signal to capital about whether Canada’s western provinces are open for the kind of investment the country urgently needs.

The through-line connecting all of these stories — the stranded mega-projects of Nunavut, BHP’s potash renaissance in Saskatchewan, the regulatory recalibration in B.C. — is the same: Canada possesses extraordinary mineral wealth at precisely the moment the world most needs it, and the country has not yet built the institutions, infrastructure, or policy frameworks to capture that advantage at scale.

Every year a world-class deposit sits stranded beyond the end of the pavement is a year Canada is not there. The question is no longer whether the country can afford to build north. It is whether it can afford not to.