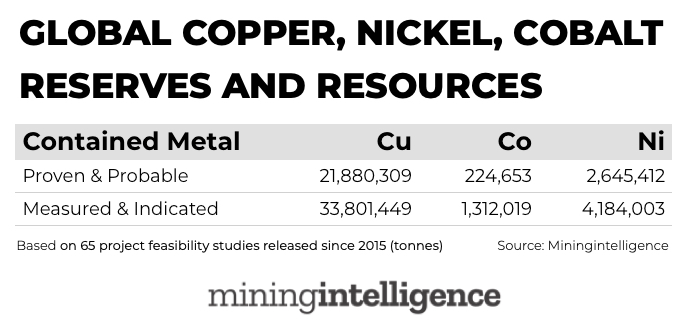

That’s only equal to a single year of global production of the bellwether metal and of course not 100% of these reserves will be extracted.

In terms of cobalt, reserves total 224.7 kilotonnes of contained cobalt at these projects, which is more than the estimated current annual production of around 130 kilotonnes.

However, projections are for annual demand for cobalt growing to more than 200 kilotonnes per year as soon as 2025 as the portable electronics and electric vehicle markets expand rapidly.

The move to nickel rich chemistries for electric vehicle batteries and a robust stainless steel industry – nickel’s number one source of demand – gives the metal a similar demand curve to cobalt.

With a modest 2.65 million tonnes of nickel outlined in the 65 feasibility studies analyzed by MiningIntelligence, exploration for nickel – and copper and cobalt – would have to step up a gear.

Click here for free Excel downloads from a database of over 37,000 projects, 16,000 companies and 2 million source documents by Miningintelligence.