Interactive infographic: The global uranium cost spectrum

Cost is as important in the economics of mining uranium as it is with precious metals. But the cost of producing uranium […]

Uranium has had its ups and downs on the spot market over the last few years. Surging demand and supply constraints elevated the price to a 17-year high in early 2024.

It was then tempered by a complex interplay between policy-induced uncertainties like tariffs and the Russia ban, shifts in investor behaviour to technology stocks, and supply dynamics among major producers such as Cameco (TSX: CCO; NYSE: CCJ) and Kazatomprom (LSE: KAP).

Now, analysis by DigiGeoData, which is owned by EarthLabs like The Northern Miner Group, has found a correlation between claims staking across Canada and the uranium price.

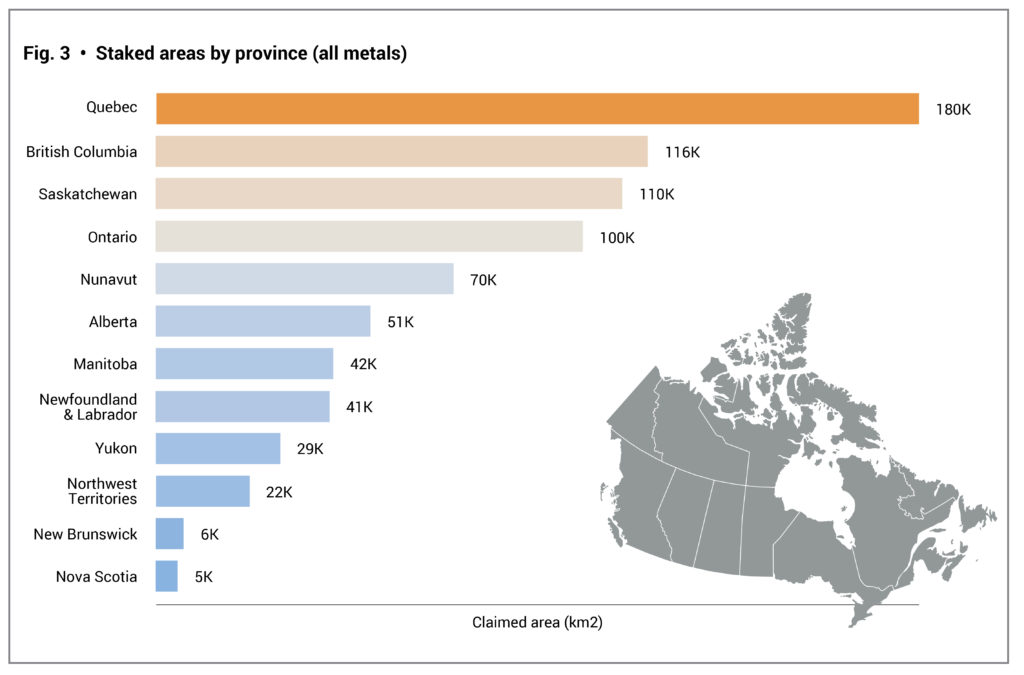

But first, let’s step back and consider the geographic distribution and dynamics of Canada’s mineral claims market, with a focus on uranium exploration.

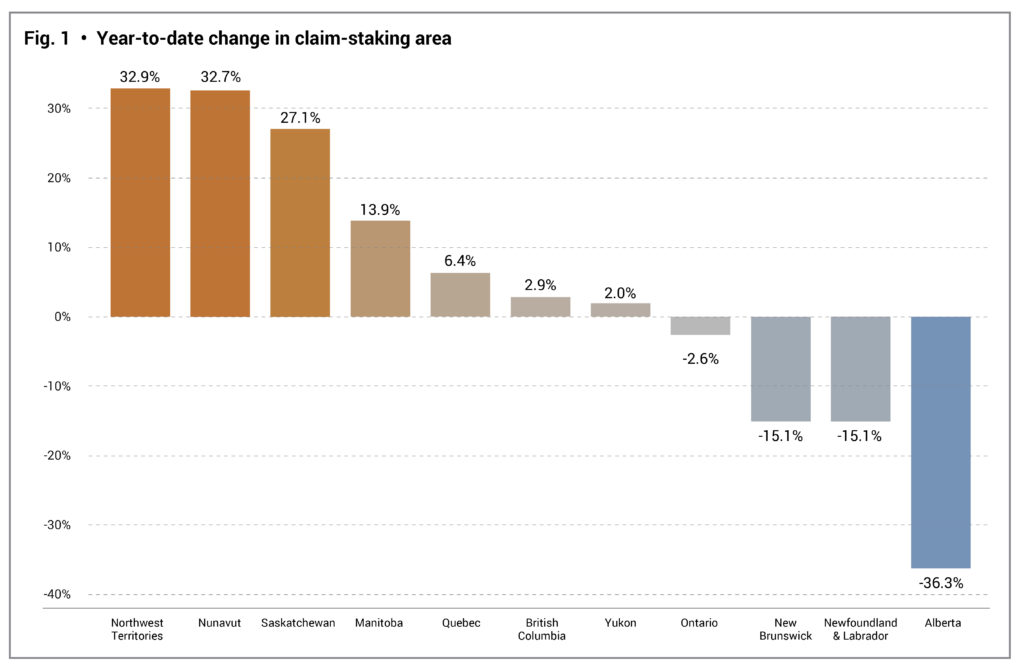

Figure 1 illustrates year-to-date staking activity, highlighting the provinces that were driving growth last year. The analysis is based on a comprehensive dataset covering Jan. 1, 2023, until Sept. 9, 2024.

Provinces historically known for uranium exploration—such as Saskatchewan—continue to lead. However, a new trend is emerging: Nunavut and the Northwest Territories are experiencing a sharp increase in staking activity, suggesting the rise of previously underexplored uranium districts.

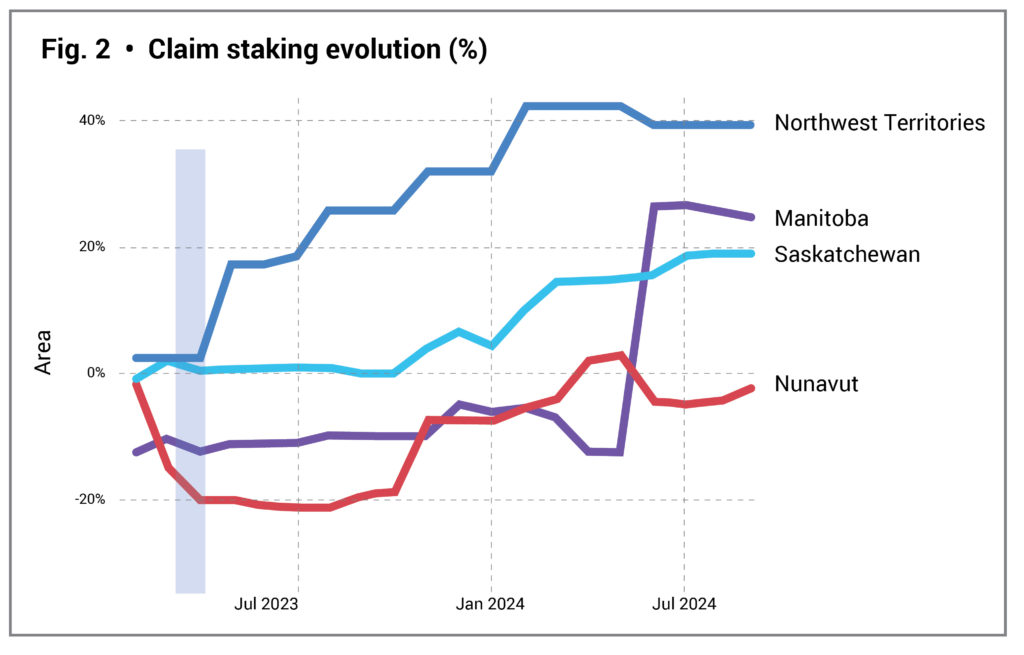

This surge closely mirrors movements in the uranium spot price. The staking rush that began around March 2023 appears to be directly correlated with price increases, supporting the idea that exploration interest in these northern territories is price-driven. These territories, referenced in figure 2 are becoming new hotspots, with staking activity responding in near real-time to market signals.

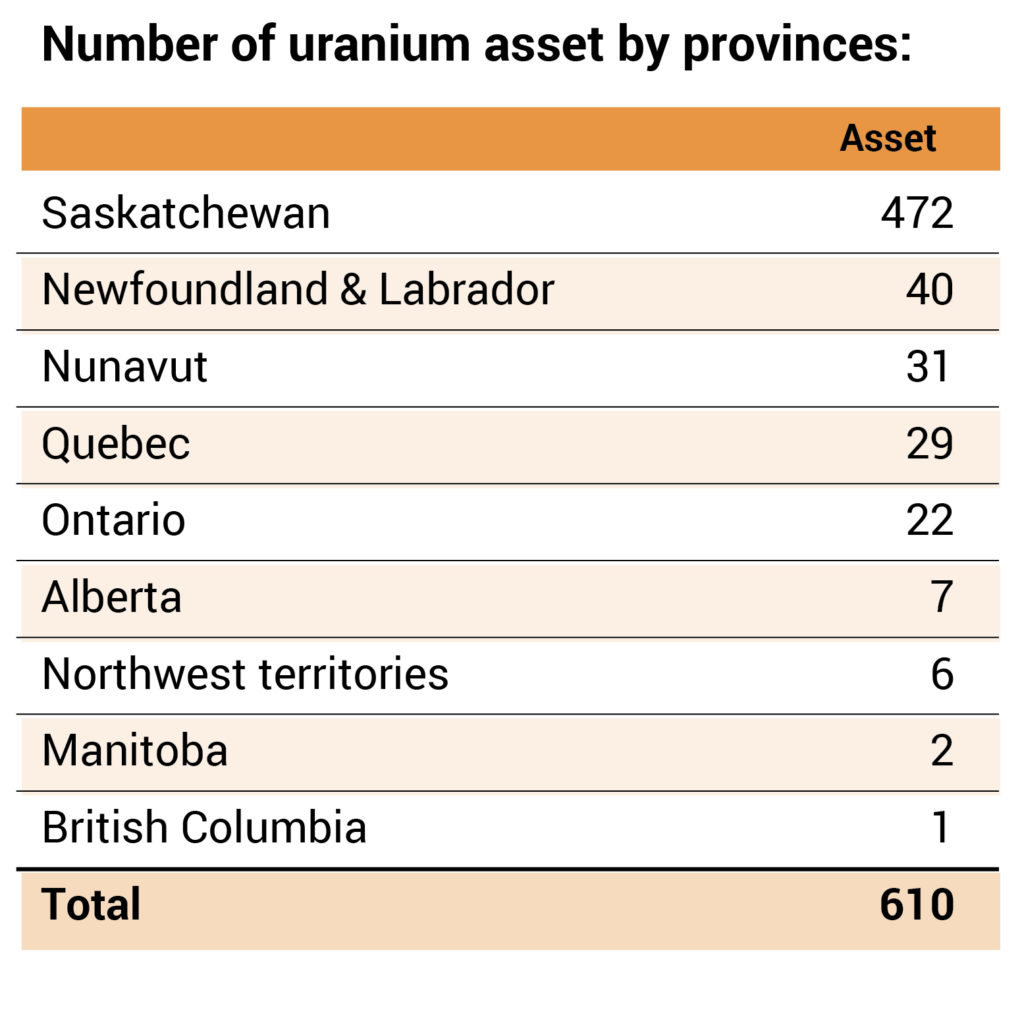

Additional confirmation comes from the number of uranium assets: Nunavut (31) and the Northwest Territories (six) still lag far behind Saskatchewan (472). However, this gap, when contrasted with current staking momentum, indicates that exploration capital is flowing into new areas in anticipation of future discovery.