Treasure Hunt: Bathurst – The camp that powered the modern world

After the launch of The Great Canadian Treasure Hunt, explorers from coast to coast have been digging into Canada’s mining past – […]

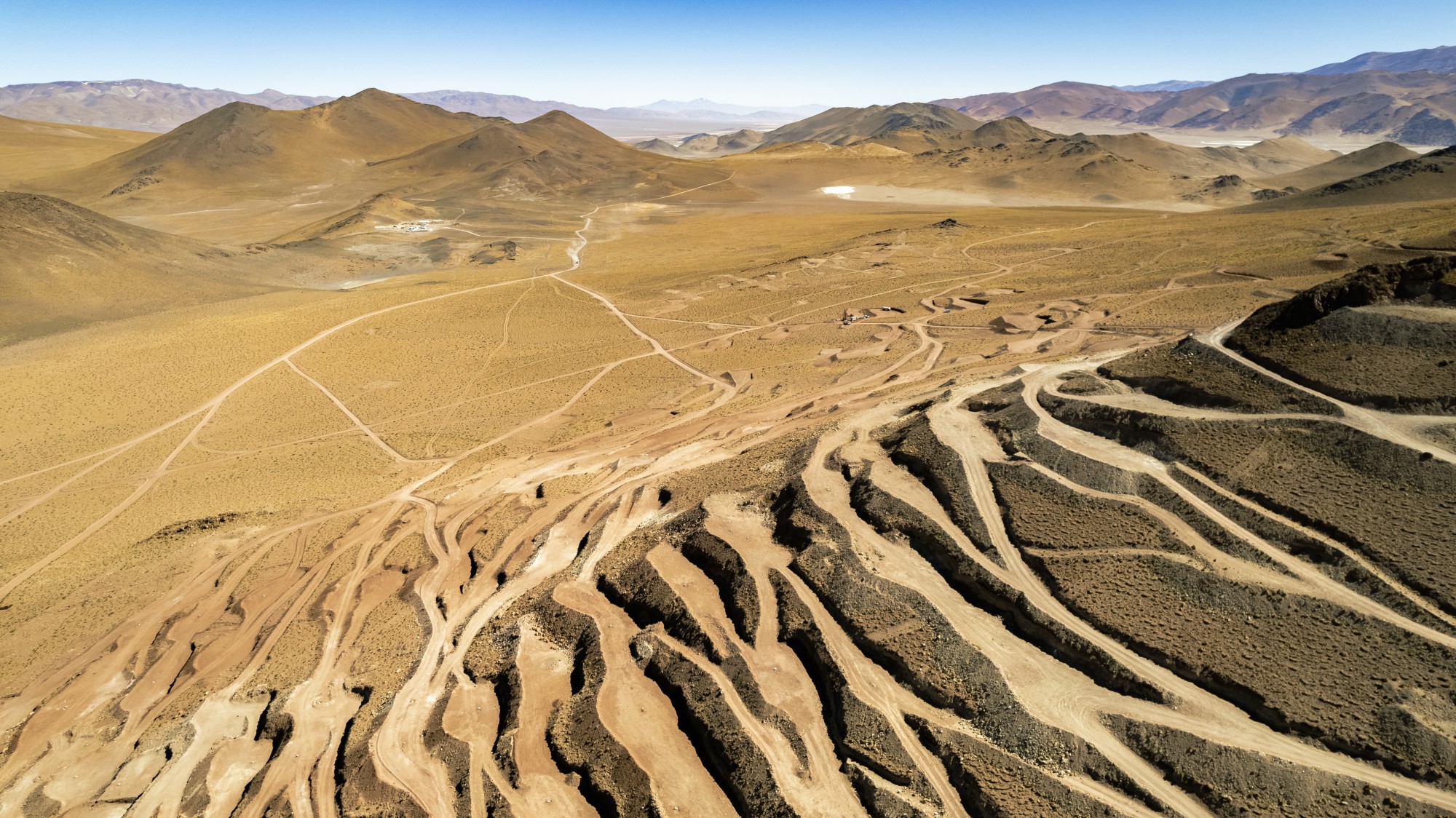

Food, energy and now minerals. In a world where competition for raw materials is only increasing, Argentina is blessed with an abundance of natural resources. But the country’s nationalist politics and macroeconomic troubles have so far prevented it from realizing its potential, especially in copper — despite its prospective geology along the Andes Mountains.

There is no doubt that the resources exist. Decades of mineral exploration have identified perhaps the largest collection of undeveloped copper projects, from First Quantum Minerals’ (TSX: FM) Taca Taca, Glencore’s (LSE: GLEN) Pachon and Aldebaran Resources’ (TSXV: ALDE) Altar. Not surprising given it shares the same geology as neighbouring Chile — the world’s top producer of the metal.

But so far only one major mine has made it into production – Glencore’s Bajo de la Alumbrera, where operations are now winding down.

Others are approaching construction decisions. Lundin Mining (TSX: LUN) has already begun early works at its Josemaria project while seeks a partner. McEwen Mining (TSX: MUX; NYSE: MUX) could list its Los Azules project in a new company to raise funds for development.

But major investments have been delayed as mining companies wait for the tangle of capital controls, import bans and export taxes imposed by successive governments to be lifted.

“Politicians here have always talked about the mineral resources, but not about the tools needed to develop them” notes Miguel Martin, an industry consultant.

Mining can work in Argentina. Investment is booming in the northwest provinces of Catamarca, Jujuy and Salta as companies from around the world race to extract lithium from the region’s high-altitude salt-flats.

While development in Bolivia and Chile — which have larger resources — has been hindered by policies designed to increase state participation, Argentina’s more laissez-faire approach should see production rise tenfold to almost 300,000 tonnes per year of lithium carbonate equivalent by the end of the decade.

In June, Lithium Americas’ (TSX: LAC; NYSE: LAC) US$1-billion Caucharí-Olaroz project became Argentina’s third lithium facility to enter production. Eramet’s US$735-million Centenario project (24,000 tonnes lithium carbonate per year) is set to enter production by mid-2024, while in August, Australia’s Galan Lithium (ASX: GLN) began construction at its Hombre Muerto West project (5,400 tonnes lithium carbonate equivalent per year) which is set to begin producing lithium chloride concentrate by mid-2025.

But what works for relatively small-scale brine operations does not necessarily work for large-scale copper projects, says Martin. With lithium prices climbing to record prices and investment costs of less than US$1 billion, lithium projects can live with tight capital controls, multiple exchange rates and tariff barriers that make Argentina one of the world’s most closed economies — all while retaining fat margins.

For copper projects with price tags of US$5 billion plus, mining companies need authorities to adopt a radically different approach to macroeconomic policy.

Such change could be coming soon.

Cut off from international markets after defaulting on its IMF loans and loath to cut spending, Argentina’s government is financing itself by printing money at an unprecedented rate.

With annual inflation running at more than 100%, the peso plummeting against the U.S. dollar and international reserves exhausted, something has got to give.

“The Central Bank today has negative net international reserves of US$10 billion, something we thought was impossible,” former Economy Minister Nicolas Dujovne said in a recent seminar. At this rate of spending, inflation could reach 200% by the end of the year, a level that risks triggering hyperinflation.

That makes this year’s presidential elections potentially the most important in a generation. They are also the most uncertain, with voters getting ready to choose between the governing left-wing coalition, the traditional centre-right opposition and a new right-wing movement which hardly existed a year ago.

The official primaries on Aug. 13th made clear how wide open the presidential elections are. In a shock result, libertarian populist Javier Milei attracted more than 7.1 million votes or 30% of the total — more than were cast for either of the two main coalitions. His beyond-the-pale prescription includes not just cutting regulation and slashing the bloated public sector, but scrapping the Central Bank and dollarizing the economy.

His success reflects the desperation of Argentineans, especially the young, not just with the country’s current predicament but also a palpable feeling of decline. More than 40% of Argentineans now live below the poverty line while fewer young people are going to university than either Chile or Peru.

As a result, whoever wins later this year will have to propose significant changes to help the economy recover. There are reasons to be hopeful.

A drought which has blighted agriculture is ending, boosting grain exports from next year. Production from the giant Vaca Muerta shale field is rising rapidly, reducing Argentina’s reliance on costly LNG imports and turning it into a major oil exporter by the end of the decade.

Attracting mining investment is also likely to play a key role.

“The good thing is that all the candidates now see mining as an opportunity. That was not the case in the past,” says Ignacio Celorrio, president, Latin America at Lithium Americas.

As expectations grow that investment conditions will improve, mining companies have begun to move their chips.

Last year, BHP (NYSE: BHP; LSE: BHP; ASX: BHP) agreed to finance $100 million worth of exploration at Filo Corp.’s (TSX: FIL) Filo del Sol, while Sibanye-Stillwater (JSE: SSW) and South32 (LSE: S32; ASX: S32) have acquired more than a quarter of the shares in Aldebaran Resources, which owns the Altar project containing 1.2 billion measured and indicated tonnes at 0.43% copper and 0.09 gram gold per tonne.

Meanwhile, Glencore has become the sole owner of the Mara project (formerly known as Agua Rica) in Catamarca province after buying out stakes owned by Pan American Silver’s (TSX: PAAS; NYSE: PAAS) and Newmont (TSX: NGT; NYSE: NEM) over the last year. Lying adjacent to the Alumbrera mine, the project could be brought into production relatively quickly.

The question will be how quickly the necessary changes can be made and if they will be sustainable.

“This could be a unique opportunity if the candidates can keep their word,” says Martin.