Spotlight: Global precious metals exploration 1

Record precious metal prices are driving global exploration for gold and silver. Here’s a list of four companies to keep an eye on. Another four companies under the global […]

This year’s Prospectors & Developers Association of Canada (PDAC) annual convention will be remembered not just for the discussions that took place in Toronto that first week of March. It also coincided with Canada’s unveiling of strong responses to United States President Donald Trump’s unfair tariffs on Canadian goods – including critical minerals.

Word at the convention was that mining and metallurgy projects in gold, base metals and rare earths are starting to attract investor attention. The 2025 convention also put Canada in the spotlight, and the federal government took the opportunity to announce that the Mineral Exploration Tax Credit (METC) would be extended for two years – great news for the mining industry.

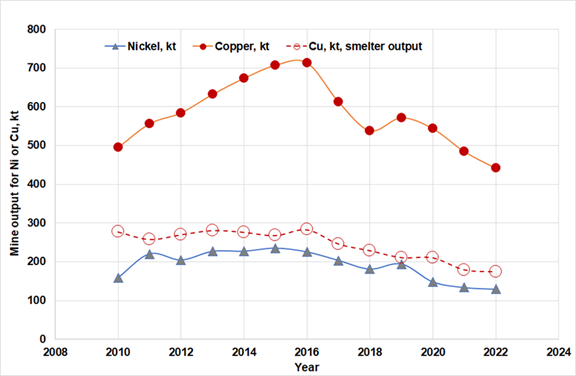

But the country needs to do much more. Canada’s output of certain critical metals is declining, and has been for years. Production (as measured by the annual tonnage of mined nickel) has fallen every year since 2014, as illustrated by Chart 1. It’s the same story for both mined copper and smelted copper. Clearly, this situation needs to change.

Across a number of sessions, speeches and discussions at PDAC, measures were outlined to help expand Canada’s production of metals – with ideas ranging from changes to mining rules, accelerated approvals and ways to help First Nations participate in the process.

While these suggestions should be acted upon, all this will take time. One of the more advanced nickel projects in the country, Canada Nickel’s (TSXV: CNC; US-OTC: CNIKF) Crawford in northern Ontario, only expects its first production in early 2028 – assuming permits are received this year.

Another new endeavour, Tartisan Nickel‘s (CSE: TN; US-OTC: TTSRF) Kenbridge project is supposed to see production from its deposit in northwestern Ontario, but it’s still a ways away. It’s a similar story with FPX Nickel’s (TSXV: FPX; US-OTC: FPOCF) Baptiste project in British Columbia. And there is no schedule as yet for the Ring of Fire projects.

So how can we increase metal output in the near and longer term? Can this even be done? While individual cases will vary, it is possible – but it will require collaboration among all stakeholders across the complete value chain.

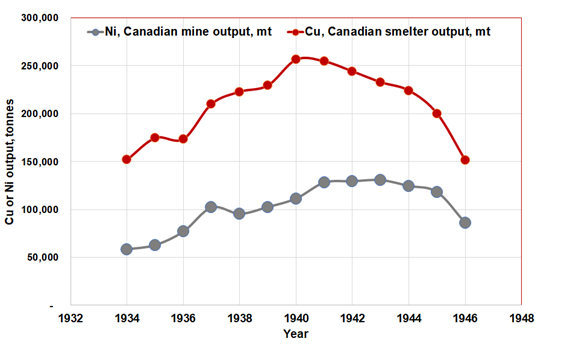

Let us go back nearly eight decades to an era of rising output in Canadian mining and smelting to see what we can learn. It’s a little-known fact that during World War II, Canada’s mining companies relentlessly raised nickel and copper production under emergency war measures – as seen in Chart 2.

Nickel output in Canada rose from about 100,000 tonnes in 1938 to about 130,000 tonnes by 1943 – a 30% increase; cobalt output would have generally followed nickel. For context, Canada produced more nickel in 1942 than in 2022.

Copper smelter output, meanwhile, increased 14% from about 220,000 tonnes in 1938 to about 250,000 tonnes a year over the 1940-42 period, though manpower shortages subsequently constrained production.

Such was the emphasis on higher and higher tonnages that the Noranda smelter in northwestern Quebec set a world record for the hourly copper smelting rate for a single furnace. It remained unbeaten across the world and over a range of technologies for nearly 40 years.

Washington’s tariffs have been described as the start of a “trade war” – and surely, this is just what it is. In the late 1930s and early 1940s, Canadian companies and governments worked alongside each other to help fight the enemy. Companies benefited from this resolve.

Could this sort of approach succeed today? Possibly. This too will take time, but with the collective will and collaboration – properly planned and equitably conducted – it could be a win-win for all stakeholders. Can the country try to repeat what we did over 80 years ago in a different war? It’s worth looking at.

In recent years, Ottawa and the provinces, likely without much pre-planning, allocated huge budgets to support a number of new electric vehicle (EV) battery plants – such that when built, they would probably use in many cases raw materials potentially imported from China, with many of the products destined for the U.S.

Two of the projects announced so far are still on track to start operating in 2026 – possibly at reduced capacity. These are the NextStar Energy battery plant in Windsor, Ont., and the General Motors and POSCO joint venture in Bécancour, Que., which will use nickel shipped from Sudbury.

However, several other projects have been postponed or possibly cancelled – including the ill-conceived Northvolt plant in Quebec, whose Swedish owner has filed for bankruptcy in Stockholm – and the Ford plant in Ontario. Last month, Honda announced it would postpone plans for a new EV plant in Alliston, Ont. for at least two years. In addition, in 2024 Umicore stopped construction of its billion-dollar plant near Kingston, Ont.

Government funding for battery plants should now be minimized in two respects. Firstly, some of these government funds should instead be re-directed to support and assist the mining industry to both expand metal output at existing plants and aid the development of new mining projects. While both have a place, manufacturing may have to temporarily take a back seat to the development of new mining and metallurgical projects.

When a mining company wishes to expand, it is prudent to first look at increasing the output at an existing facility instead of building a brand new mine and surface plant, which would require significantly more capital. The higher throughput also lowers the unit cost. Of course, each mine and situation is different and needs to be examined individually, but this option for Canada should be investigated.

Perhaps some form of government support could encourage such expansion projects, keeping in mind metal prices. We only need to look at the results achieved by Canadian mining companies during war time in the 1940s. To succeed today, it would take the same type of collaboration amongst the parties that occurred back then.

Secondly, Canada will then be producing more materials and products that the world needs – and in fact materials that the U.S. desperately needs and cannot produce itself. This is not like automobile or battery production, where the U.S. can adapt and probably produce more at home.

For example, U.S. reserves of nickel (and cobalt) are very small, meaning that the U.S. cannot produce its own primary metal. Also, the U.S. cannot produce enough primary copper and must rely on imports. The U.S. does have large reserves of the red metal, but it will take a very long time for the country to significantly expand its primary copper output.

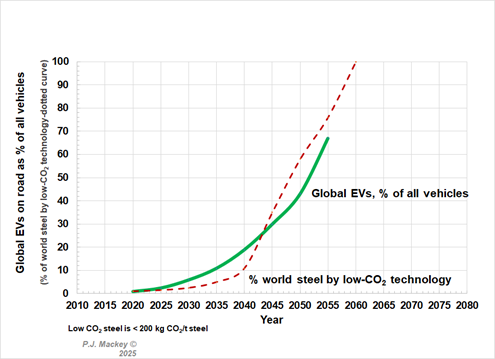

As we look towards the future, it is postulated here that the uptake of EVs will likely be quite slow and that batteries will not be needed at the rate that governments originally estimated. The author projected in his 2021-2022 John F. Elliott Lecture that the rate of increase in the number of global EVs as a percentage of all vehicles would in fact grow at a much slower rate from pre-2020 than what carmakers and governments expected – as seen in Chart 3.

While growth is expected to gradually pick up by about 2040, demand for batteries will be quite slow as well in the short and medium term. As a result, any government investment in battery plants and the like should reflect this slower rate of EV pick-up. Of interest, Chart 3 also shows a similar slow growth rate for steel made with low-CO2 technology. As things stand now, steel production and the global vehicle fleet each produce some 8% to 10% of global CO2 emissions.

In conclusion, Canada will need resolve and collaboration among stakeholders to boost the output of certain critical metals. A new national vision will be needed to ensure the full development of Canadian critical minerals – similar to what occurred during the wartime years.

Canada can already count on good mineral reserves and a solid technology base in mining, smelting and refining. When you add liquified natural gas and oil from Alberta, the country is ideally located to play a central role in global trading – thanks in part to mine output.

Besides the ideas discussed at PDAC 2025, measures to boost interprovincial trade (also under discussion) will help build a new industrial supply chain. To help us get there, education at all levels will need a boost. We will also need, as has occurred before, to attract outside talent.

If such reforms are indeed put in place, I have no doubt that Canada can reach its full potential.

Phillip John Mackey, born in 1941 in Australia, is a renowned metallurgist recognized for co-developing widely-used copper smelting processes. He was inducted into the Canadian Mining Hall of Fame in 2022.